Let’s ask a question that seemingly has an obvious answer. Why is estate planning important?

First of all, when many hear the term “estate planning,” they quickly envision those who own mansions, various real estate holdings, large stock portfolios, expensive toys, and priceless heirlooms. Please, put that stereotype out of your mind. Everyone should have an estate plan or a will. There are several reasons, but let’s touch on the most important. Your wishes are carried out, and you can prevent or discourage fighting among potential heirs by spelling out what each beneficiary will receive.

You decide—not a court, and thereby prevent the ugliness that could easily follow.

Many folks understand this, but common mistakes can surface, thwarting your intentions. And they can surface after it’s too late for you to do anything about it. Before we jump into some of the common missteps, let’s acknowledge that estate planning can be complex. Much will depend on your estate and the assets you plan to gift to your heirs.

But mistakes, if not avoided, can lead to costly consequences that could have been circumvented with proper planning. That said, we’d be happy to entertain any questions or point you in the direction of an experienced estate planning attorney. As always, feel free to consult with your attorney.

Here are seven common mistakes to avoid.

- Not having any plan. Have you ever had a project you wanted to complete, but procrastination set in? Once completed, you feel a sense of satisfaction. It’s like checking the box on your to-do list.

What happens if you die without a will, which is known as dying intestate? For starters, you haven’t legally documented how you want to distribute your assets. If that happens, the courts will determine who gets what, and it will rarely coincide with your intentions.

Besides, it can turn into a messy and expensive process if acrimony arises among potential heirs. - Set it and forget it. Creating an estate plan isn’t something you set up and forget about. You’re not on autopilot after signing the document. If major life events occur, you should revisit your plan. You may have had additions to your family, a divorce can change the familial equation, or your net worth or assets changes over time.

Have you moved to another state? State laws impact how wills are drawn up, and a new address may require an updated legal document. - Doing it yourself with a will won’t cost you much, and there are plenty of online options. But are you comfortable navigating unexpected complexities that may crop up? For example, does the online site fully take the laws of the state where you reside into account?

I sometimes like to say, “You don’t know what you don’t know.” Another way to frame it: Do you know the right questions to ask? If not, your will might not have the proper language because it wasn’t written in the correct manner.

Saving money on the front end could be costly to your estate if the will you initially prepared hits unintended hurdles. - Do account-specific beneficiaries contradict the written intentions in your will? I’ve discussed the need to update beneficiaries, if appropriate. But what happens if a bank or brokerage account lists one beneficiary or beneficiaries and your will names another?

For example, let’s say an IRA account at ABC Brokerage has your two sons listed as your beneficiaries split 50-50, but the will explicitly states your daughter as the heir of the account. In this case, your sons will win the battle. Please be sure the wishes in your will line up with the beneficiary forms that are held with your financial institution. - Did you forget to fund your trust? There are complexities in setting up a trust and we encourage you to seek a qualified professional, but let’s review one unfortunate mistake.

While a living trust can ease the transfer of assets to beneficiaries without going through probate, it’s not enough to simply create a trust. You must transfer assets into the trust.

If you fail to fund the trust, the assets you intended to pass smoothly to your beneficiaries won’t pass smoothly at all. Instead, the situation will create headaches and needless legal fees for your heirs. In addition, your assets may not wind up in the hands of the intended beneficiaries, as you thought you had spelled out. - Making DIY changes. You know what changes you want. But adjustments executed improperly can lead to unwanted consequences that muddy your intentions. Once-valid legal documents may be inadvertently sullied by do-it-yourself changes that may only be straightened out in lengthy legal proceedings.

- Planning for your minor children. This is my last point, but it’s definitely not the least important. A major reason for end-of-life planning is not only to properly bequeath your assets after you pass, but to be sure your minor children, if you have any, are taken care of. Be sure to have a guardian in place. Make sure you inform the guardian and receive consent. Spell out instructions regarding financial matters to that person. Too often, the guardian has too much freedom with your money.

Final thoughts

Creating and implementing an estate plan will allow your wishes to be carried out when you are no longer here. However, don’t throw up roadblocks that can create complications, delays or even thwart your plans. If you have any thoughts, ideas or questions, we’re simply a phone call away.

New high is October—what drives the overall market?

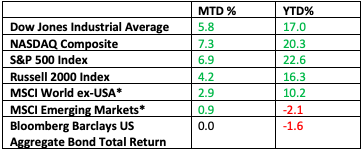

Following a modest sell-off in September, stocks racked up a big gain in October, with the Dow Jones Industrial Average and the S&P 500 Index setting new highs late in the month, according to market data provided by the St. Louis Federal Reserve.

The S&P 500 turned in its best monthly performance of the year, while the Dow managed its best return since March.

Key Returns

While October’s rebound is encouraging, let me caution that I want to keep you focused on your longer-term goals. Stocks have historically had a long-term upward bias, but they don’t move in a straight line, no matter how positive the economic fundamentals may be.

Be that as it may, 2021 has been a very good year for investors, as the table of returns above illustrates. For the layperson, viewing the multiple highs we’ve seen this year can spark questions. One may ask, “Why are stocks performing so well? Aren’t we still in a pandemic? Isn’t inflation a concern? Aren’t we facing economic and political challenges that should derail the rally?” All are good questions. All are fair questions.

But various metrics that investors collectively follow vary from what the casual observer might be more attuned to. And by investors, I mean the millions of large and small investors that buy and sell equities on a regular basis.

Let’s look at three variables that have played an outsized role in this year’s rally:

- economic growth

- profit growth

- interest rates

They have all been strong tailwinds for stocks.

Economic growth slowed in the third quarter, but overall, it has been strong this year. Economic growth by itself might not be an important variable, but economic growth powers profit growth. And investors are very attuned to what happens with profits.

The pandemic has created enormous economic distortions that have benefited some sectors at the expense of others. I get that. Overall, however, the economic rebound has fueled a substantial increase in earnings this year, according to Refinitiv, and that has aided equities.

Notably, October’s strong performance was closely tied to another quarter of much-better-than projected Q3 profits (Refinitiv). Think of it like this. If you find a small business that you might want to purchase, you’d examine many aspects, but current profits and expected future profits would play a big role in the final purchase price. The same line of thinking holds true for publicly traded companies.

Let’s add one more variable to our recipe: interest rates. Interest rates and bond yields are at very low levels. Without jumping deep into the weeds of time-tested academic research, low interest rates leave savers with fewer options. In turn, that makes stocks more attractive to savers.

In Conclusion

I’ve said before that we’re due for a correction of at least 10%. Obviously, that did not happen in October, as favorable economic fundamentals countered September’s uncertain mood.

Yet, risks never completely abate, even if they are overshadowed by favorable developments. Inflation is still a worry, and investors now expect a faster pace of rate hikes from the Fed, according to a recent CNBC survey. Even if the Fed were to go ahead with one or two quarter-percent rate hikes next year, the fed funds rate would remain near historic lows.

I trust you’ve found this review to be educational and informative. Let me emphasize that it is my job to assist you. If you have any questions or would like to discuss any matters, please feel free to give me or any one on my team a call.

As always, I’m honored and humbled that you have placed your confidence and trust in me to serve as your financial advisor.